Posted June 01, 2026

By Nick Riso

For Whom the IPO Bell Tolls (SpaceX)

IPOs go up on day one. Everybody knows that.

The company prices the night before, opens at a pop, the founders ring the bell, and the financial press writes the same story they always write about the next era of American enterprise.

It's practically liturgical.

Jay Ritter, a finance professor at the University of Florida who has spent 30 years studying nothing but new issues, puts the average first-day return at roughly 18% going back to 1980. During the dot-com bubble, it hit 65%.

So, the number on the screen in large green type isn’t a fiction. It's just that you can't have it.

It belongs to the institutional allocations, the roadshow relationships, and the accounts that got stock at the offer price the night before.

By the time the market opens, you are, quite literally, the exit.

And once you're past that first day, the data gets quietly brutal — the average IPO underperforms the market by more than 3% annually across its first five years.

Hold one for three years past opening day, and you finish with $0.83 for every dollar a comparable established company earned you.

This is also not a secret. It’s taught in business school and ignored by almost everyone who has ever stood in front of a laptop at 9:30 a.m., finger hovering, waiting for the market to open.

Is There an IPO Soon?

SpaceX is listing on the Nasdaq under the ticker SPCX, targeting a raise of up to $75 billion at a valuation of approximately $1.75 trillion.

To understand the scale: Saudi Aramco's 2019 offering, previously the largest in history, raised $29 billion. SpaceX is doing two-and-a-half of those in a single day.

The company's bankers are Goldman Sachs, flanked by more than 20 other banks on the underwriting syndicate — a number that feels like more an act of geopolitical mobilization than a deal structure.

The company is, in very technical accounting terms, losing money.

The S-1 shows a net loss of $4.9 billion in 2025, with another $4.3 billion gone in just the first quarter of 2026, losses that trace back to the integration of xAI and X and the ongoing burn of Starship development.

Starlink, the satellite internet division, is profitable and growing. I recently read somewhere that SpaceX is just an internet company that also does rockets. It’s true!

Everything else is an act of faith, at least for now.

Elon Musk owns roughly 42% of SpaceX and controls approximately 79% of the voting power through super-voting shares.

The public offering floats about 5% of the company. That's the part you get to own. That's the part that votes as 0.5% of the company's actual governance weight.

In the old language of capital markets, this is a liquidity event for insiders wearing an IPO's clothes.

Should You Own It? Well, Here’s the Thing…

Here's the part that should genuinely alarm the retirement-account-holding citizens of this country: Whether you want to own SpaceX or not, you probably will. And you probably won't have been asked.

The mechanism runs through index rules, something most people think of as boring.

Nasdaq, which runs the Nasdaq-100 index that underlies the QQQ ETF, changed its inclusion methodology effective May 1 of this year.

The old rules required a newly public company to season for anywhere from three to 12 months before qualifying for inclusion. The new rules created a "fast entry" path. Any company large enough to crack the top 40 Nasdaq-100 components by market cap gets included 15 trading days after IPO.

SpaceX is worth more than the entire airline industry multiplied by nine. It will be, on day one, among the five largest components of the Nasdaq-100. Then 15 trading days after June 12 — roughly July 6 — the index rebalances, and every QQQ holder in America becomes a SpaceX shareholder.

QQQ alone holds $385 billion in assets as of this writing.

The full Nasdaq-100 ecosystem — index funds, structured products, derivatives, benchmarked institutional accounts — exceeds $1.4 trillion.

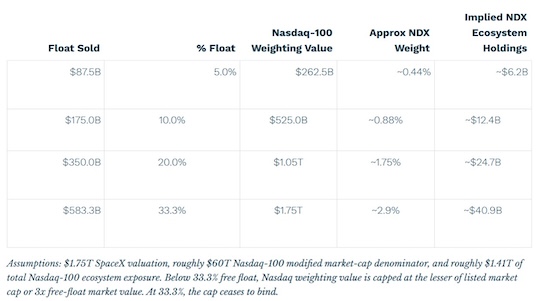

Using the float-adjusted methodology Nasdaq adopted alongside the fast-entry rule, SpaceX will carry a weight of roughly 0.44% at the initial 5% float. That translates to approximately $6.2 billion in forced Market-on-Close buying on a single rebalancing day.

This guarantees that existing money tracking that index will have to sell a whole bunch of other things in order to buy this new slug of SpaceX.

Every dollar in QQQ is already deployed. There is no idle cash sitting around waiting for a good idea.

To buy SpaceX, the fund sells Apple. Sells Microsoft. Sells Nvidia. Proportionally trims every existing holding, turns those proceeds into SPCX, and hands them to whoever is willing to sell at whatever price clears on that afternoon.

The word for this, in market structure language, is "forced buying." The word for the people on the other side of it — the ones who knew it was coming and positioned accordingly — is "front-runners."

The Old Lock-Up

None of this happens in a vacuum. The lock-up structure SpaceX filed with the SEC reads less like investor protection and more like a sophisticated float-management program optimized around the index mechanics.

Enrique went over this last week. (Read that here.)

Under a typical IPO, insiders are prohibited from selling for a uniform 180 days. SpaceX abolished that standard and replaced it with a cascade. After the Q2 earnings release — expected sometime between mid-July and September — up to 20% of eligible insider shares can be sold.

If the stock trades 30% above the IPO price for five of any 10 consecutive trading days, another 10% unlocks immediately. Then five time-based tranches kick in at days 70, 90, 105, 120, and 135 — each releasing another 7% of eligible shares. Another 28% comes loose after Q3 earnings. The remainder at 180 days.

Run that arithmetic, and you realize that by the time Nasdaq conducts its September 21 quarterly rebalance, a meaningful chunk of the originally locked-up shares may be freely tradeable.

Which means the float grows. Which means the Nasdaq-100 weighting, which scales with float under the new methodology, grows with it. Which means another wave of forced mechanical buying by every passive fund in America, triggered automatically, announced in advance, and exploitable by anyone with a Bloomberg terminal and a basic understanding of how index reconstitution works.

Source: etf.com

At 5% float, the Nasdaq-100 ecosystem needs to hold roughly $6.2 billion.

At 10%, it doubles to $12.4 billion. At 20%, it reaches $24.7 billion.

At full float of 33%-plus, QQQ and its cousins will need to absorb $40.9 billion in SpaceX exposure — without anyone's consent.

Every share the insiders sell on the open market ratchets up the weighting, which ratchets up the next rebalance buy, which hands the sellers a deeper pool of captive institutional demand.

The insiders don't need to time the market because the market will be timed for them.

So What?

The academic literature on what happens to stocks around index inclusion is fairly clear.

Additions rise into the rebalancing date, then tend to underperform afterward as the mechanical buying pressure dissipates.

Robin Greenwood and Marco Sammon at Harvard documented this across decades of S&P 500 additions. Morningstar research confirmed the pattern more recently. Stocks tend to enter indexes near their relative peaks, and the funds that track them cannot do otherwise. The index systematically buys high.

What makes SpaceX categorically different from any prior inclusion event is the combination of three factors operating simultaneously — a genuinely historic dollar magnitude of forced buying, a float so constrained that the mechanical demand represents nearly ten percent of available shares on day one, and a staggered unlock schedule that converts every subsequent insider sale into another round of index-amplified demand.

What’s worse here is that the S&P 500 is also reportedly considering rule changes, cutting the seasoning requirement from 12 months to six and potentially relaxing financial viability standards for megacap listings.

The S&P's float-adjusted methodology limits the damage somewhat; SpaceX would get capped at a fraction of its nominal weight until the float expands. But the direction of travel is the same.

The world's most important index — one with $13-plus trillion tracking it — is rewriting its rules to court a company that loses more than five billion dollars a year.

The justification, when one is offered, runs something like this…

Modern private markets allow companies to grow for decades before going public, so the old seasoning periods don't make sense anymore.

This isn’t wrong, exactly.

It’s the kind of argument that’s technically coherent and practically devastating — the rhetorical equivalent of saying the speed limit should be raised because modern cars have better brakes, then watching the accidents happen.

Where We Go From Here

On Thursday morning, June 12, SPCX will open for trading. The first-day pop will almost certainly be spectacular.

CNBC will put the number on the screen in large green type, someone will ring the bell, and the founders will look satisfied in the way that people who are worth tens of billions of dollars tend to look on the days they become worth more.

And 15 trading days later, on a quiet Monday afternoon in late June, while most people are thinking about something else entirely, trillions of dollars in passive index funds will execute their rebalancing trades.

They will sell fractional slivers of Apple, Microsoft, Nvidia, and 97 other companies. They will buy SpaceX at whatever price the market has determined, into a float barely wide enough to absorb the demand, from sellers who have known this trade was coming since May 1.

The retail investor who owns QQQ in their 401(k) will not be notified or asked. Their account will simply, one morning, reflect a small position in a rocket company that loses five billion dollars a year and is worth more than Australia.

IPOs used to be how companies raised money to go build things. The dot-com boom, for all its madness, averaged IPO sizes of $100 million — companies going public to fund operations, not to provide exit liquidity for the people who got in early.

FDR signed the Securities Act of 1933 with a speech about people who seek to draw upon other people's money being "wholly candid regarding the facts."

He meant it as a minimum standard. For SpaceX's passive-investor army, it may not even clear that bar.

The gravity well of a $1.75 trillion company is strong enough to bend the rules of the indexes around it.

What comes after the mechanical buying subsides — when the float is fully unlocked, when the index weight is fully loaded, when the insiders have sold what they came to sell — that's the part the academics have been studying for 30 years.

The long-run data is not encouraging.

Sign Up Today for Free!

Truth & Trends brings you market insights and trading tips you won't find anywhere else — unless you have your own personal hedge fund manager on speed dial...

Meet Enrique Abeyta, one of Wall Street’s most successful hedge fund managers. With years of experience managing billions of dollars and navigating the highs and lows of the financial markets, Enrique delivers unparalleled market insights straight to your inbox.

In Truth & Trends, Enrique shares his personal take on what’s moving the markets, revealing strategies that made him a star in the world of high finance. Whether it’s uncovering the next big trend or breaking down the hottest stocks and sectors, Enrique’s insights are sharp, actionable, and proven to work in any market condition.

Inside these daily updates, you’ll gain:

- 50 years of combined trading wisdom distilled into actionable insights.

- A behind-the-scenes look at how Wall Street pros spot opportunities and avoid pitfalls.

- Exclusive strategies that Enrique personally uses to deliver exceptional returns — no fluff, just results.

To have Truth & Trends sent directly to your inbox every weekday, just enter your email address below to join this exclusive community of informed traders.

Don’t miss your chance to learn from one of the best in the business.

Sign up now and take your trading game to the next level.

Reports of Software's Death Are Greatly Exaggerated

Posted May 29, 2026

By Greg Guenthner

SpaceX IPO: When EXACTLY to Buy

Posted May 28, 2026

By Enrique Abeyta

Everyone Knows the Market Is Rigged. But How?

Posted May 22, 2026

By Greg Guenthner

The Death of Laissez-Faire Capitalism

Posted May 21, 2026

By Enrique Abeyta

Welcome to the Dark Side of the Moon

Posted May 20, 2026

By Nick Riso